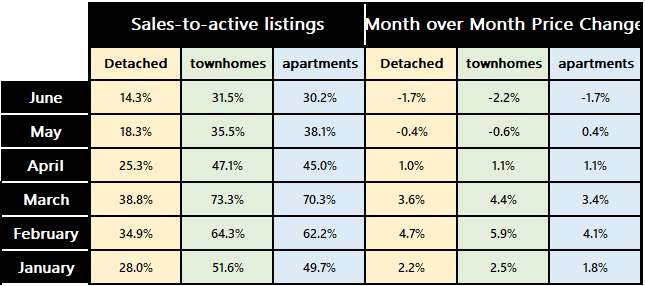

The Metro Vancouver real estate sales numbers continue to slow. For this past June the sales numbers are 35% below last year and 23.3% below the 10-year average. The main reason for the drop in sales is the higher interest rate. Inventory has stayed relatively tight. There were 5,256 new listings which is a 10.1% decrease compared to June 2021 and a 17.6% decrease from May 2022. The total number of listings is 3.8% lower than June of 2021 but a 4.1% increase compared to May 2022. As you can see from the table below, the sales-to-active listings ratio continues to decrease which translates to decreasing property prices. The typical explanation is the downward pressure on home prices occurs when the ratio dips below 12% for a sustained period while home prices often experience upward price pressures when the ratio is above 20% for several months.

For Detached homes the sales-to-active listings ratio was 14.3% with a month over month decline in benchmark price of 1.7%. For townhomes the ratio was 31.5% and the price delay was 2.2% for the month. For apartments the ratio was 30.2% and the price decline for the month was 1.7%

There was an enormous amount of real estate and economic news that is casting a huge cloud of negativity over the markets. More and more people are forecasting recessions but nobody really knows how bad and how long the recession will be. And the forecast for when it will occur range from 4 years from now to “it is already happening”.

The gist of the problem is that central banks in the developed nations have been propping up the economy with unusually low interest rates since the Great Financial Crisis in 2008. A lot of the increase in asset prices such as real estate and stocks are due to this. It was fine for a long time until the covid pandemic when the stimulus was just too large and too untargeted. It caused a huge increase in asset prices that eventually creeped into everyday necessities. Then people realized that it was inflation. Now the central bank has to decide how much to increase interest rates to bring inflation to a manageable range without cratering the economy. Currently, gas, oil, commodities, 5-year bonds and consumer sentiments are all going down. If recession is coming, maybe they won’t raise the interest rate much more. But nobody knows right now. Not even the central banks. They will act accordingly as the data comes in.

If you are buying your home to live in, then the ups and downs of the market should not be your main focus. First, you are saving on rent. Second, nobody knows how the price will move. Vancouver is a very special place. It has the best climate in one of the best countries to live in. Also, Canada has an aggressive immigration policy and most of the new arrivals will gather around Vancouver and Toronto. But it is hard to separate reality from fear mongering.

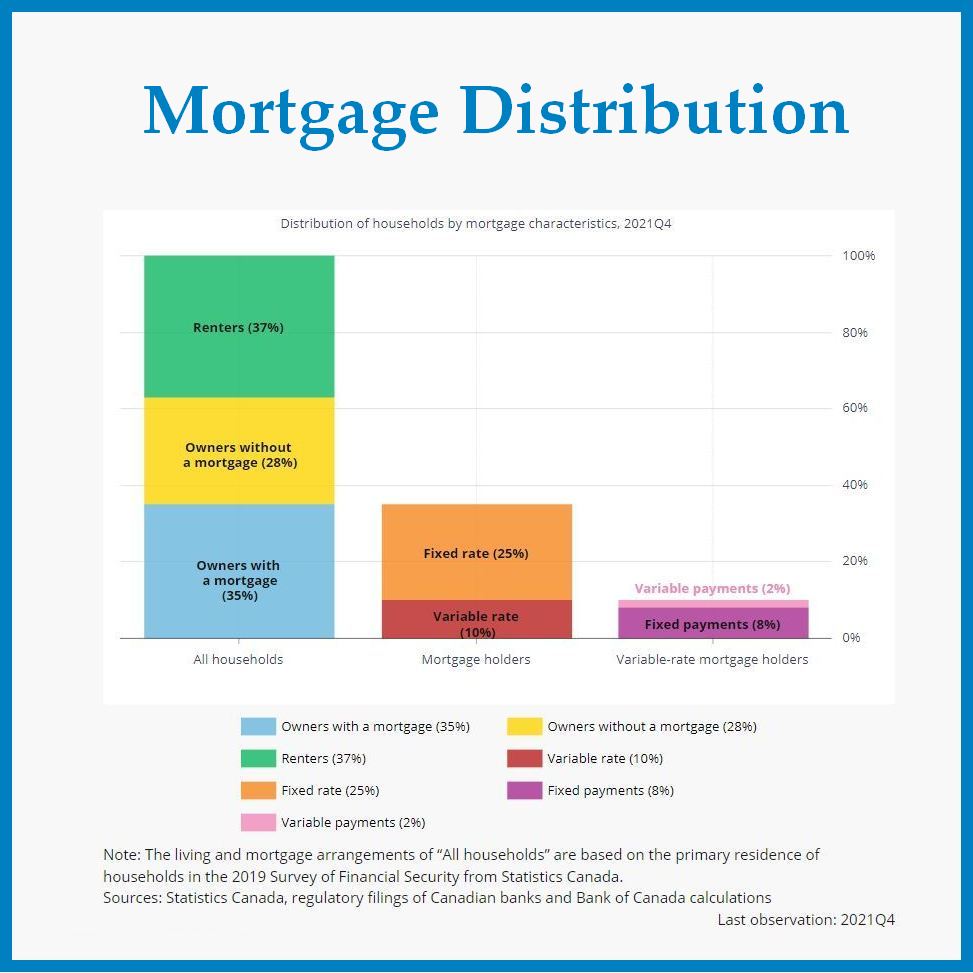

Manulife recently released a survey with some shocking results. I have included a graphic summarizing some results. If you want to see the rest of the report here is the link: https://www.manulifebank.ca/personal-banking/plan-and-learn/personal-finance/spring-debt-survey.html?.

The report said almost 25% of the homeowners say if the interest rates increase further, they would be forced to sell. But before you think there is going to be a big sale coming, if we dig deeper, I think we can conclude this number is wrong.

The report said almost 25% of the homeowners say if the interest rates increase further, they would be forced to sell. Considering the Bank of Canada meeting is next week and it is expected that they will increase the overnight interest rate by 0.75%, you might think there is an opportunity here. But before you go and find a realtor, let’s look a little deeper.

From a Bank of Canada report, we know that only a third of the households in Canada have a mortgage. About 28% of them have a variable rate mortgage and of those, only 20% have a variable rate mortgage where the monthly payment will change with the rising prime rate. This means only about 6% of the mortgage holders have to worry about raising payments before the maturity of the mortgage. So not 25%. And of this 6%, there should be many who can tolerate the increased payments. And many expect the higher interest rate environment to be short lived so the rate may come down before the mortgage matures. So, it is not as bad as the survey suggests. If you purchased a place to live in and you have a job, then you’ll be fine.